Sunday

Lunchtime: My co-manager, Pras Jeyanandhan, pings me a message on WhatsApp.

We had woken the day before to the news that the US had launched its much-anticipated attack on Iran. By Sunday the news was full of images of burning buildings in Tehran as the impact of “Operation Epic Fury” became clear.

We chatted back and forth for half an hour or so: what was the reaction in crypto markets, how much are oil futures up? The Saudi and Egyptian stockmarkets were open and trading down about 2% giving us a useful datapoint on how European markets might react in the morning.

We switched our attention to the portfolio. The fund has slightly elevated levels of cash after some recent sales. Which positions are at risk in a market meltdown? Could there be some opportunities in the coming week to deploy some additional capital?

We agreed to see how the market opened on Monday and then reassess. It was going to be an interesting start to the month.

Monday

Surprisingly the European market opened relatively calmly. Most of the moves seemed rational. Equinor and Repsol, two big European oil stocks, were up strongly. The airline majors were getting hammered. Our fund was down as well but less than the overall market. Our defence names, such as Alzchem and Indra, were holding the portfolio up offsetting some of our smaller companies which were under pressure.

Pras and I discussed if we should adjust the portfolio but decided to hold off making any knee jerk trades.

See also: Fund manager diary: Mike Sell

The regular firm-wide investment call was at 11am – Iran was naturally at the top of the agenda. The UK, Global and North American fund managers had obviously been doing the same as us – examining their portfolios for unexpected risks but also looking for opportunities.

Nobody was sure how the conflict would play out but the prevailing view was it would probably be short lived and unlikely to derail any long-term company specific theses. But equally, nobody seemed keen to jump in with fresh capital at that exact moment given the uncertainty.

Tuesday

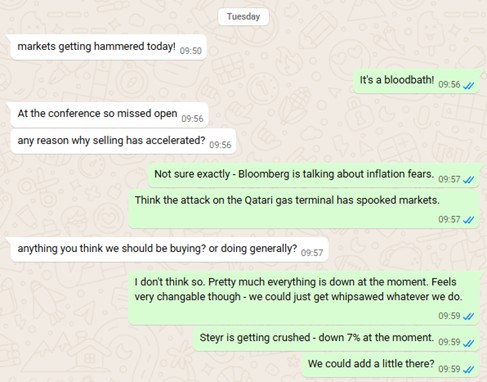

The US attack on Iran has come on a busy week for us. For the next three days, Pras and I were booked to attend the annual Berenberg EU Opportunities conference in London. This is a fantastic event focused largely on European small and mid-cap stocks – our bread and butter. Although representatives of several of our holdings would be attending, we were mostly looking for new ideas.

Pras messages me after his first meeting, feeling a bit blind as he wasn’t in front of his computer. Unlike Monday, the markets were much worse today, as fears increased a prolonged conflict could lead to inflation and possibly even a recession. Energy-intensive Europe was feeling the brunt of the fears.

Steyr Motors is an Austrian defence company we had owned for some time. Think of them like the Ferrari of defence – low volumes of premium priced customised motors. The results they published back in February were encouraging and they had won some contracts recently which improved their outlook.

Pras and I had been discussing over the past week about adding to our position as the already cheap shares hadn’t really moved on the news. I give Pras a call to discuss and we decided to add 25bp to our position – not a particularly heroic move but one which felt sensible – taking advantage of the fact that, as a small-cap stock, Steyr was getting caught up unfairly in the market selling.

Pras and I were feeling a little bruised after a tough spell of performance in February and keeping on top of the fast-moving market was quite exhausting. At least the fund was regaining some relative performance this week.

Wednesday

I’m still feeling under the weather, so Pras has to fly solo again at the conference. Ironically, most of the meetings we’d scheduled today were with European defence companies – Exosens, Theon International, Colt CZ Group and Exail Technologies.

Pras’ debrief comment at the end of the day was “valuations in some cases are looking very extended, but I’m even more bullish on the underlying demand picture”. Of course, we are not the only investors looking at defence as a theme. The hard part of our job is finding ways to play the huge increase in spending without overpaying on valuations.

We discussed the oil price impact on Europe. I’d been looking into where oil was stored. It turns out the problem was that much of it was trapped on the wrong side of the Strait of Hormuz. Pras wondered about Vopak – a Dutch company we have owned in the past. They own oil storage facilities in strategic locations around globe including Shanghai, Singapore, Rotterdam and Houston. Perhaps one long lasting impact of the current conflict will be that storage of oil derivatives will be structurally higher, providing more of a buffer in times of geopolitical turmoil such as this. Could be an interesting angle to pursue.

Thursday

Full of paracetamol, but feeling a lot better, I catch up with Pras at the conference. Four companies to meet today.

The most interesting was Frequentis AG – an Austrian small cap we’ve never looked at before. They had caught our eye as they are a leading provider of air traffic control software, both civilian and military. There is a real opportunity for them in the drone space – increasingly strategic assets need to be protected from drone attacks, both deliberate and accidental. Frequentis seems to have developed a good solution to the problem. Valuation looks rich potentially, but the idea is interesting. Definitely one to research more.

Friday

The market seems to have finally calmed down a bit, and even recover slightly. Pras and I debrief with our thoughts on the conference, exchanging views and information.

One take away from the meetings was just how much capex was going into upgrading the electricity grids around the world. Europe, and Germany in particular, is leading the charge backstopped by (German Chancellor Friedrich) Merz’s fiscal expansion programme. We have several holdings in this area already, but decide we will continue to look for other ways to get exposure.

Some relief as the market closes for the week, but plenty of stress — screens full of red as indexes surrender most of their year-to-date gains in a few brutal days.

It has been an exhausting week. We’ve been analysing the portfolio for risks, but also for oversold opportunities; weighing the threat of prolonged conflict in the Middle East, energy disruption and the knock-on impacts against President Trump’s well-documented ability to flip the narrative in an instant and trigger a risk-on rally. Our contrarian instinct says add, but we conclude it’s probably too early.

We are also coming away from the Berenberg conference with a shortlist of compelling ideas that warrant further work and could eventually find their way into the fund. Markets may be closed for the weekend, but with President Trump promising yet more ferocious attacks, we’ll be monitoring developments closely. For now, though, a well-earned gin and tonic and some rest before we go again next week.

Data source (unless otherwise stated): Bloomberg.