Even before the effects of the coronavirus outbreak tore through global markets, the European economy was on shaky ground. But for Carmignac’s Mark Denham, being a bottom-up stockpicker means he can still source resilient companies across the continent.

Denham joined Carmignac three years ago after 12 years with Aviva Investors, and in that time he has been running the €269m (£235m) Carmignac Grande Europe Fund, a pan-European Sicav. For the past nine months he has also led the FP Carmignac European Leaders Fund, launched as an Oeic for the UK market in May last year.

The two funds follow more or less the same strategy except that European Leaders is ex UK and an Oeic structure. “FP Carmignac European Leaders has only been going for nine months, so we have to use the experience, track record and what we’ve done on Grande Europe as our reference point,” says Denham.

Keeping screen time to a minimum as markets reel from Covid-19

As a stockpicker, Denham is not fond of addressing macro issues in interviews but he accepts Covid-19 has been so invasive in financial markets that he must make an exception. It comes as no surprise to him that markets have reacted so negatively to the outbreak, given they hate uncertainty. “It’s hard to know exactly what the short-term damage to profits and sales is going to be because things are changing on a daily basis,” he says.

“And it’s even harder to predict what the longer-term implications might be for companies.

“The authorities, whether they’re monetary or governments, are responding to varying degrees around the world. It’s all very supportive but I think until one of the western markets plateaus in the number of new cases of coronavirus, it’s hard to see stock markets reacting in a sustainably positive way.”

With such dynamic movement of markets, Denham is reminding himself not to screen watch but to get on with the fundamentals of the job: analysing companies. However, he is confident in the resilience of the companies the fund invests in, saying the process means the team homes in on businesses with high sustainable profitability that reinvest for growth: businesses that can “grow to some extent under their own steam”. “I don’t want to be too cavalier about it but one hopes the long-term damage to their franchises won’t be that much.”

Year to date the Euro Stoxx 50 is down by 28.8%, while the broader Stoxx Europe 600 is down 24.6% in sterling terms, but Denham argues that while there is no one particular area of opportunity, the drop has created entry points for a range of the portfolio’s holdings. “At the margin we’ve been using cash to add to some of our holdings, just as the prices have come down.”

Denham says with reporting season ending a couple of months ago, there has not been a lot of bottom-up specific corporate news as everything is about the effect of coronavirus.

“But day to day, we just carry on, me and my analysts. We have a shortlist at any given moment of about six names we are working on.”

Luxury powerhouses versus tech titans

The team looks for businesses that have two key characteristics: high sustainable profitability and the reinvestment of profits internally to grow the business for the future. The combination of those two factors results in a compounding effect in the value of the company over time, according to Denham.

The team screens 1,600 companies from across Europe based on different factors around profitability and reinvestment.

But that’s just a starting point, says Denham. “Ninety per cent of the work we do is traditional fundamental analysis of meeting management to understand the business drivers and do our valuation.”

In terms of sectors, Denham says despite the obvious lack of technology leaders, Europe has a lot to offer and is an overlooked region. “Clearly, Europe hasn’t benefited from the internet business model explosion over the past 20 years in the same way that other regions have. We don’t have a Facebook or Google that dominate the world; we don’t have an Alibaba, Tencent or Mercado Libre that you would find in emerging markets.

“But let’s not overlook the fact that in Europe we do have amazing businesses. For instance, luxury goods companies LVMH, Hermes, Adidas and Puma.”

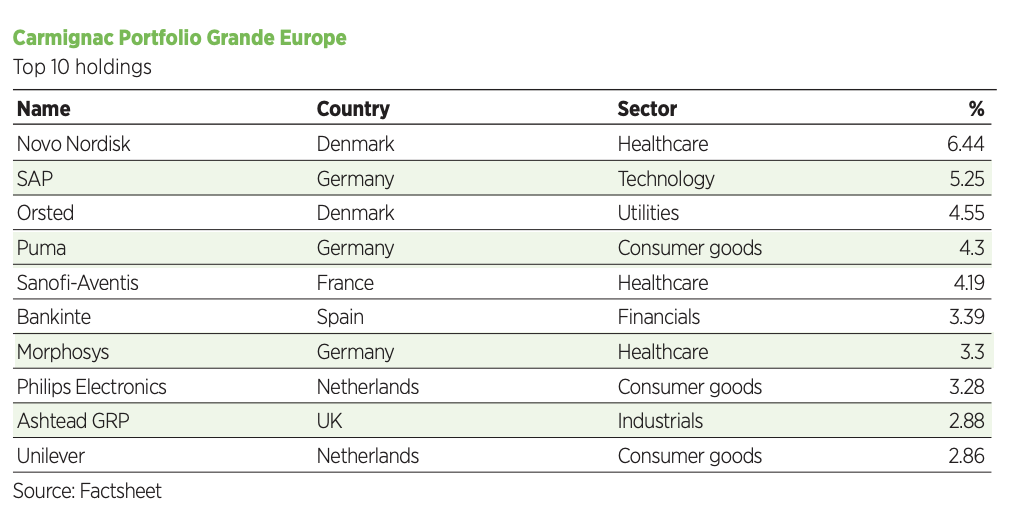

Puma is the fourth-largest position in the Grande Europe fund, accounting for 4.3% of the portfolio.

Europe may not have tech titans but Denham draws attention to niche players in the tech space such as semiconductor company ASML and German software provider SAP, which is the second-largest position in the portfolio at 5.25%.

Denham also believes European companies lead the world in renewable energy and the theme accounts for about 10% of the portfolio. “That’s the next mega-trend for the next few decades,” he says. The portfolio contains Danish wind turbine company Vesta but he also highlights Siemens Gamesa and Orsted as key players in the space.

“In addition there are solar plays,” he adds. “We have a solar farm developer called Solaria in our portfolios, so in Europe we can really tap into this mega-trend for the future.”

The European market by market capitalisation is dominated by or has large exposure to sectors Denham just does not find interesting. These are banks, insurance, utilities, telecoms, oil and which, in aggregate, account for nearly 40% of the European market by capitalisation.

“You have to be fully active in Europe to avoid those sectors. Our active share is above 90% so we don’t follow the benchmark at all.”

An area the team particularly likes at the moment is biotech because of its diversified pipeline, which Denham thinks is underappreciated by the market. About 8% of the fund is exposed to this sector. “Businesses here such as Morphosys, Galapagos, Argenx have multi-billion euro market caps. We’re not talking about a Neil Woodford-type strategy of investing in illiquid names. We could sell our holdings in a couple of days.”

SRI criteria applied once universe has been whittled down

All funds at Carmignac integrate ESG but Denham’s strategies are also classed as socially responsible.

They have low exposure to carbon reserves and carbon emissions and exclude sectors such as weapons, tobacco and gambling.

Once the financial screen has whittled the universe down to about 500 names, the SRI criteria are applied, which further reduces the pool to about 400 stocks. From this group the team picks about 35 to 40 holdings after conducting fundamental analysis. Denham likes the portfolio to be concentrated and it has just 36 holdings currently.

He only ever looks to change about six or seven holdings in each year if deemed appropriate.

“If you have 100 stocks, first of all you’re not going deliver performance better than the benchmark and, second, you can’t follow them all. Above 40 becomes counterproductive; below 35 and you start to get a little bit too concentrated, almost like a focus fund.

“There’s more going on in Europe than meets the eye but, for whatever reason, we have ended up with a quite high concentration in Denmark.”