The vast array of methods used to benchmark funds-of-funds products means it is confusing to compare products and judge performance, but portfolio managers believe there are ways to help investors make informed decisions on these products.

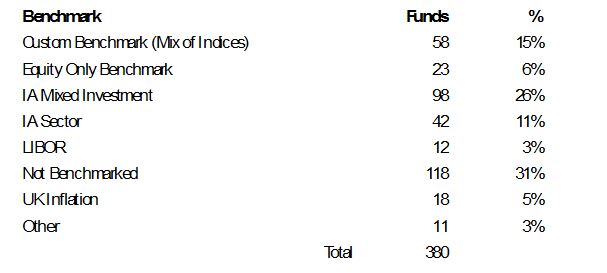

A Morningstar report looking at 380 UK funds identified six different methods of benchmarking and said the fact the funds in the universe are made up of different asset classes and have different weights assigned to them makes comparing between products problematic for the end investor.

It found 31% of funds did not have any listed prospectus benchmark which is said makes it hard to form expectations around performance and difficult to measure success.

Peer group comparison

The most common way to benchmark these products was to use the average performance of an Investment Association sector such as the IA Mixed Assets peer groups. It found 37% of funds in the UK market chose this method – 26% used one of the IA’s mixed assets sectors and 11% used another IA sector.

However, it said that peer comparison is not always the best way to assess performance. “If funds in a peer group are performing badly on average, a strategy that is performing better than peers may end up being the best of a bad bunch.”

Using a composite benchmark

The second most popular is a custom composite benchmark that blends mainstream bond and equity benchmarks in a proportion that is in line with the fund’s long-term asset allocation. Morningstar found 15% of funds used this approach and said while intuitively it looks like a better solution, it too is by no means perfect.

“Firstly, the fund groups have complete discretion over how they create these benchmarks and it can be hard to tell if they have chosen the correct benchmark that truly represents their investment universe. Quite often these benchmarks are very basic in their construct, and not reflective of the fund’s objectives and scope.

“On the other hand, some managers may choose a more granular approach by including as many as eight indices within them which doesn’t make it simple and easy to comprehend.”

It concluded this approach makes it harder for investors to compare funds effectively and loses the whole attraction of benchmarking all together.

The other forms of benchmarking identified by Morningstar included Libor, used by 3% of funds, inflation plus X%, used by 5%, and using a level of distribution/income, which it said can be useful for investors looking for absolute return.

Benchmarks used by 380 UK funds-of-funds

See also: Asset managers shunning Libor but inflation-plus still preferred benchmark for absolute return

AJ Bell flags issue in value for money report

It comes as AJ Bell flagged the issue in its value for money assessment published this week. The platform provider’s fund board raised concerns about assessing multi-asset funds on performance, stating “no single financial instrument or index represents a fair benchmark”.

AJ Bell head of active portfolios Ryan Hughes (pictured) describes benchmarking multi-asset funds as “a real challenge”. “There are many bad ways of doing it and there is no one good way of doing it,” he adds.

“Our funds are in the IA sectors,” he says. “We think that’s an OK starting point. We fully accept it’s not perfect, but it’s a relatively broad based comparator.”

Hughes says one has to accept there will be some variability in returns when you compare anything to such a broad based sector.

“If you’re an equity fund investing in UK equities, the ‘Look what you could have won’ is what did an ETF give you? That’s nice and straightforward. But in the world of multi-asset there isn’t that equivalent to assess if you’ve done a good or a bad job.”

The pros and cons of using a composite benchmark

Momentum Global Investment Management portfolio manager and co-head of research Alex Harvey says one advantage of using a composite benchmark is it allows for attribution to asset allocation around that composite, and can flag how well managers are performing in that regard, and if they demonstrate skill and add value with asset class selection.

But, he adds on the downside these composites tend to be modelled on historic relationships and returns which may hold less well or be inferior when looking forward.

“In the current climate with near or below zero sovereign bond yields, you need to build diversification in using multiple levers, be that through asset class, styles and manager selection,” he says.

Liontrust prefers internal comparisons among multi-manager range

Liontrust Asset Management head of multi-asset John Husselbee says rather than judge portfolios against different strategies across the market, he finds it more meaningful to compare each portfolio against the rest of the portfolios across Liontrust’s range.

“In doing so, we can be sure that each portfolio achieves two objectives over the short, medium and long term. First, that they target the outcome expected by investors in terms of the level of risk, as measured by volatility, in each model portfolio. This helps advisers align clients’ risk profiles with an appropriate portfolio.

“Second, it maintains a focus on maximising the return for each model portfolio while still targeting investors’ level of risk. This means the higher the risk of the portfolio, the greater the potential for volatility, positive returns on the upside and losses in down markets.”

Using risk as a gauge

Hughes suggests the fact many multi-asset strategies target a level of risk adds another layer of complexity to determining what a good outcome is.

“Is it staying within your risk band and producing a decent return? Or is it producing a slightly higher return but going slightly out of your risk band? And then when you compare that to other people, who do you compare it to? Funds that are trying to apply the same risk band?”

Husselbee says comparisons to peers or composite benchmarks do very little towards answering the question of how closely a portfolio maps an investor’s attitude to risk, but Liontrust places attitude to risk at the heart of its proposition.

“Asset allocation should be determined by how much someone is prepared to lose and by how much they want to gain and not by a portfolio’s potential to outperform a peer group or benchmark over a defined period,” he says

Hughes suggests while it’s incredibly difficult for investors to compare multi-asset products, what they can do is look under the bonnet of these funds at how much risk is being taken and the active and passive exposure and avoid looking at past performance.

Husselbee adds: “The best way to determine the success of a multi-asset vehicle is whether it meets its stated objective and in doing so, delivers an outcome aligned to a client’s risk/return expectations.”