An increasing number of conventional funds are being repurposed as ESG or sustainable, but fund buyers have warned asset managers that there is more to changing a mandate than slapping a new label on a fund.

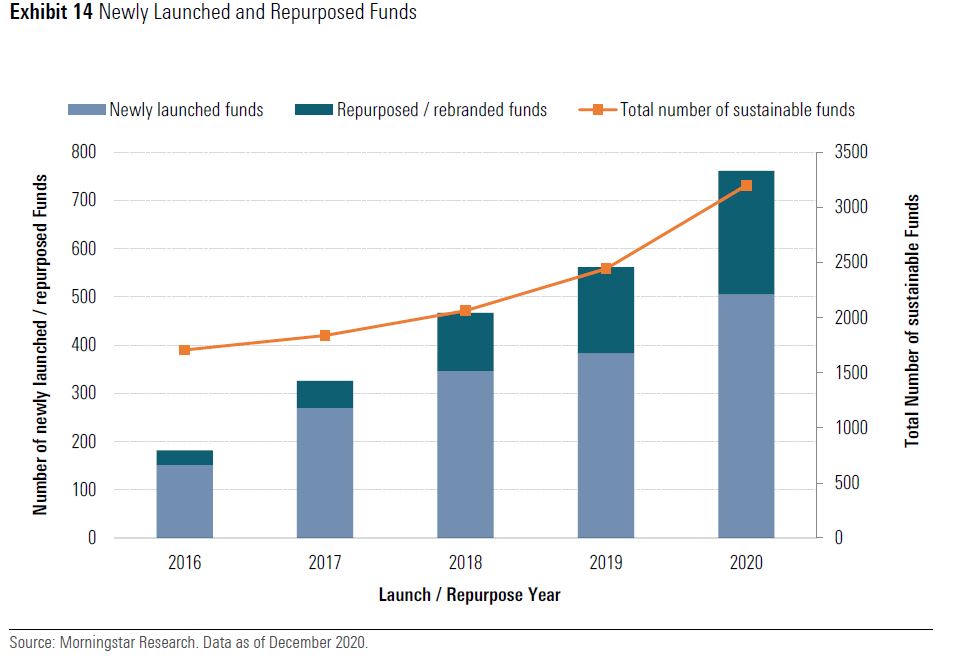

According to Morningstar data published in February, 256 funds repurposed or rebranded as sustainable in 2020, up from 179 the year before. In Q1 this year alone, the number was already at 127.

Morningstar said: “Transforming existing funds into sustainable strategies is a way for asset managers to leverage existing assets to build their sustainable-funds business, thereby avoiding having to create funds from scratch.”

It added repurposed funds that rebrand typically add terms such as ‘sustainable’, ‘ESG’, ‘green’, or ‘SRI’ to their names to increase visibility among investors looking to invest more sustainably.

“This may also be a way for fund companies to reinvigorate ailing funds that are struggling to attract new flows.”

Last month, Invesco announced the Invesco Pan European Structured Equity fund, managed by Thorsten Paarmann and Alexander Uhlmann in Frankfurt, was being renamed the Invesco Sustainable Pan European Structured Equity fund to reflect the embedded ESG criteria into the strategy’s factor-based style.

“As our research deepens, we constantly evolve alongside our clients, believing there are new risks and opportunities that can provide better protection to the fund,” Paarmann said at the time. “This is why we’ve made the decision to make changes to the fund’s strategy and to embed ESG criteria explicitly into the existing process.”

In January, Fidelity repurposed the Fidelity European Opportunities fund as the Fidelity Sustainable European Equity fund. It said it changed the investment policy to incorporate a sustainable investment focus and the fund now forms part of its Sustainable Family range.

‘If you just stick a sustainable badge on, you’re going to face questions’

Fidelity head of UK wholesale John Clougherty says for a fund to be considered in its Sustainable Family of Funds a strict threshold ESG rating criteria is applied.

“In some cases, these strict requirements have led to significant portfolio change through the process of repurposing, while in others it might be more of a natural evolution.”

He adds: “When we undertook a review of the underlying holdings of the Fidelity Sustainable European, they were close to being fully able to be sustainable anyway because the portfolio manager was already ESG-focused, with a large weighting towards higher rated sustainable stocks in the portfolio.”

On communicating such changes to investors, Clougherty says: “I think you have to be really open about it – show clients that either a thorough review has taken place or a genuine attempt to change the fund into a truly sustainable offering.

“If you simply change nothing and just stick the sustainable badge on, you’re going to face a lot of questions.”

Market accepting ESG as a material investment consideration

EQ Investors senior sustainability specialist Louisiana Salge (pictured) thinks the recent increase in rebranding funds is a consequence of the general market accepting ESG risks and opportunities are material investment considerations.

Salge also thinks that EU regulation is starting to have an effect. The Sustainable Finance Disclosure Regulation (SFDR), part of the EU Sustainable Finance Action Plan, started to be rolled out across Europe in March which stipulates reporting requirements for market participants in relation to ESG products.

“From our perspective as a fund selector with longstanding sustainability expertise, it is great to see innovation and ESG moving into the mainstream,” she adds.

‘Fund titles mean next to nothing’

But Salge says “fund titles mean next to nothing” because EQ’s own research has revealed some funds without any ESG branding having better ESG integration than some specifically marketed as such.

“It is crucial to cut across messaging and analyse the fund investment process, the team’s philosophy, its resources and oversight and also dig into underlying holdings to really get security over a fund’s objectives regarding sustainability.”

Salge also points out that converting to ESG/sustainability is not a uniform change to process – there are different shades and ambitions when it comes to investment sustainability objectives, and fund selectors should be clear on theirs.

She points to the EQ Positive Impact portfolios which aim to allocate to fund managers following best practise impact investing, allocating capital to those businesses solving social and environmental needs.

“That is hugely different to a fund screening out a few sectors or screening out businesses with lower ESG scores,” she adds.

Similarly, LGT Vestra head of sustainable portfolios Phoebe Stone has observed lots of funds being repurposed but urges caution when selecting them for portfolios.

“One needs to be extremely thorough through extensive qualitative analysis to ensure philosophy of the fund does match up with the mandate,” she says. “We would need to see evidence of experience within the team, depth of research, authenticity and understanding of the complex subject matter to consider a fund.

“Clearly it needs to be more than just a new label going on a fund.”