Last year saw risk assets in redemption mode – as I cover in more detail in Everything Flows, Refinitiv Lipper’s review of the UK fund market in 2022. The last two months of 2022 did finish on a more positive note, however, with both equities and bonds in the black. Nevertheless, with the twin perils of inflation and recession casting a shade over markets, it is instructive to see how investors have been responding … and where they might be heading. So, first, what has been happening over the past year?

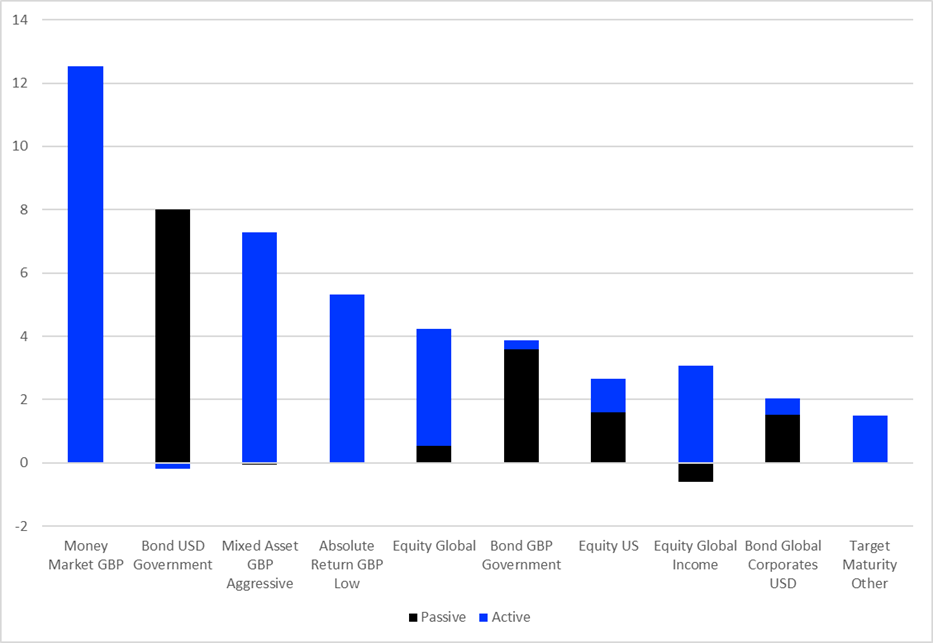

Chart 1: 10 Largest Positive Flows by Lipper Global Classification, 2022 (£bn)

Source: Refinitiv Lipper

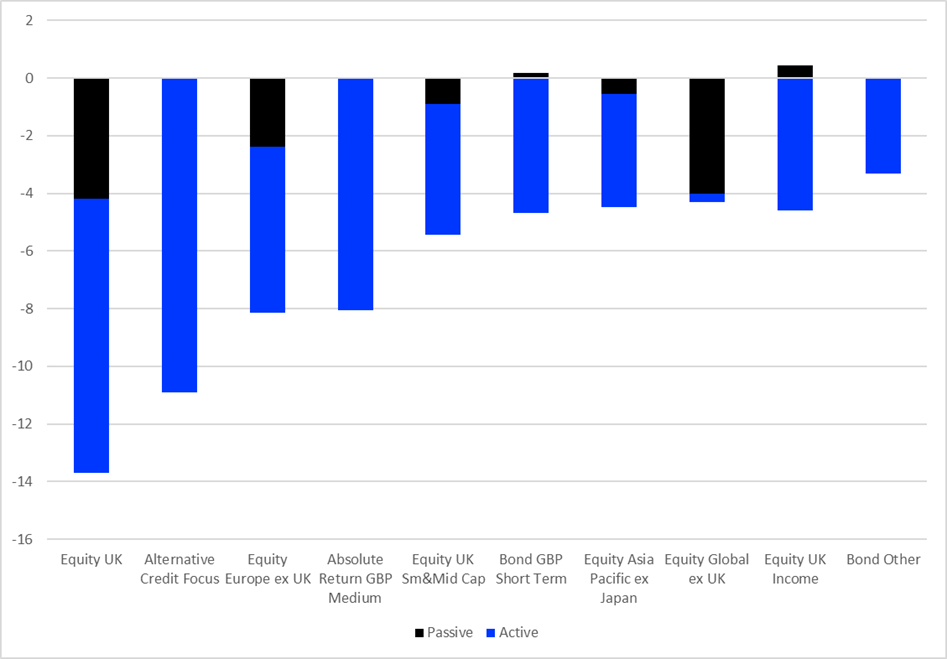

Chart 2: 10 Largest Negative Flows by Lipper Global Classification, 2022 (£bn)

Source: Refinitiv Lipper

We will pass over the money market influx, which is down to pension funds buying in the wake of the September mini-budget. UK investors have bought into government bonds – particularly the US – and have continued to sell down UK equities, of pretty much any flavour, despite a decent relative performance over the past year.

Government bonds are the ultimate safe-haven asset, particularly in recessionary conditions. The strengthening dollar over the first three quarters of the year will also have added to the attraction of US government bonds. The US is ahead on the rate-tightening cycle, and investors may well have taken a view that most of the rate-induced pain is in the past – in the process, disregarding Fed warnings of further hikes. These safe havens may turn out to have rocky bottoms if rates rise – in which case, there is more pain to come.

Turned out nice again?

I see little benefit in trying to second-guess either the Fed or the Bank of England – and, as economist JK Galbraith observed: “The only function of economic forecasting is to make astrology look respectable.” Still, while I am not in the business of prediction, I will share with you a couple of things that worry me – niggling my reptile-like hind brain – despite the emerging optimism, sprouting like snowdrops through the frozen ground, that things might after all not turn out too bad after all.

The first is the consumer – and the UK consumer in particular. If you are sitting on a mortgage, the cost of this has risen markedly over the past year. If you are a private renter, that will have been passed on to you in the form of higher rents. Many people were already maxed out on these payments before all this hit.

My other, related, worry is whether this is the year the zombies finally rise up and start taking chunks out of investors. It is not that I have been taking the work of George A Romero a little too literally, but how these same rising rates may impact the so-called ‘zombie companies’. These have interest-coverage ratios below one and have kept staggering on since the global financial crisis because of the cheap money its resolution necessitated. As borrowing costs rise, that medication is being withdrawn.

How much should we fear these zombies? Depends on who you ask. Some estimates put them at about a fifth of the US’s 3,000 largest publicly traded companies, carrying about $900bn (£735bn) of debt. On the other hand, the US Fed reckons: “Zombie firms are not a prominent feature of the US economy” as they “are few in number and generally small, [accounting for] a small share of total credit to nonfinancial firms.” So, choose your fighter.

So far, there has been little impact. “The net percentage balance for changes in default rates on loans to corporates increased for small businesses, slightly increased for medium businesses, and was unchanged for large businesses in Q4,” says the BoE Credit Conditions Survey – 2022 Q4. However, “These were expected to increase for businesses of all sizes in Q1.”

Financing conditions are expected to remain tight, and businesses that have difficulty in passing on rising costs are more vulnerable to default. As a result, no one seems to be tipping high yield in this environment.

Default risk is lower for investment-grade funds. That said, there is a discernible shift to better-rated credits in the corporate space. As an example, Bond GBP Corporates’ exposure to BBB-rated credit – the lowest investment grade rating – went from an average of 42.3% in 2018 to 49.9% in 2021, before falling slightly to 48.3% last year.

Missing links

One inflationary asset that did not work last year was the inflation-linked bond. I have gone on at some length, not least here, as to how spiking rates punctured inflation-linked bonds’ claim to be the quintessential place to hunker down in times of low/negative growth and rising inflation.

That may be great in theory but, in practice, duration destroyed values, particularly in UK linkers. This may still be an asset to return to if inflation remains elevated but stable, combined with insipid or negative growth: in other words, stagflation. If this happens, it will be the greatest comeback since Ali v Foreman’s Rumble in the Jungle. And – if only because no-one seems to be calling it – perhaps it might.

Other options include infrastructure companies. These tend to perform well during inflationary periods, as the underlying assets often have charging structures linked to inflation. Performance in 2022 was reasonable, both in terms of flows and returns, with the Lipper Global Classification of Equity theme – infrastructure attracting £900m of UK investor cash and returning 2.1%. While that is certainly below inflation, it is above global equity returns.

Another possibility is commodity funds. These saw outflows of about £380m last year, but Commodity Blended funds returned 18.5% – the third-best by classification over the year. They are an asset class sensitive to inflation but also vulnerable to negative growth. It is feasible, however, that even with sluggish growth – if supply bottlenecks keep demand above supply, as happened last year – this could still perform, particularly where these bottlenecks persist most.

Property is an asset that is held to be a good inflation hedge, with many commercial rents linked to inflation. But how well does it hold its value in recessions? UK investors have been negative on the asset class for some time, with £2bn withdrawn from property funds in 2022, the sixth consecutive year of redemptions (amounting to -£16.8bn). What is more, it has not been as bad a year for bricks and mortar as for others (Real Estate UK returned -7.4% and Real Estate Global -4.2%).

The best case is that the world skirts recession and growth rebounds. On the other hand, rate rises may fail to rein in inflation, but still push the economy into recession. Reading the tea leaves of recent fund flows, it looks like investors are rebalancing portfolios after a turbulent year, with a bias towards higher grade bonds, implying low growth and stabilising, if not falling, inflation.