It may seem counterintuitive that in a year of extreme volatility, both economically and politically, that markets within the United States should have consistently remained as one of the few bright spots for investors.

The performance has largely been driven by the strength of US equities, which despite an initial sell-off in March, recovered sharply – and at the time of writing – continue to offer mainly positive returns. These have been concentrated in a few sectors and industries, mostly driven by technology stocks in the ‘Faang’ companies; Facebook, Apple, Amazon, Netflix and Google. Yet with the presidential election – already set to be one of the most politically divisive in modern times – due to take place on 3 November, it begs the question how much more volatility can the markets stand?

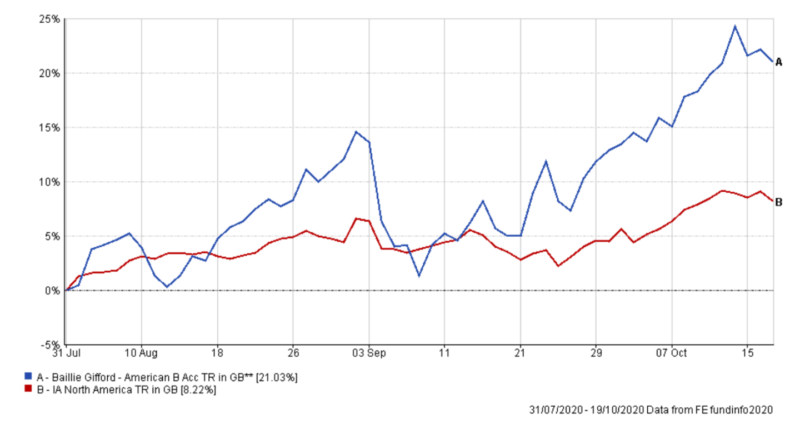

While the obvious answer is that no one can predict the future, in the short term essentially, we can expect a period of inertia while the machinations of the election play out. As the chart below shows, towards the end of the summer performance in the markets – even among the tech stocks – saw signs of stalling, as the impact of the first post-Covid stimulus package (The CARES Act) began to drop off. Baillie Gifford’s American fund, which holds strong positions in technology and online retail stocks, is one example of a fund falling sharply in mid-September, before rallying again towards the end of the month:

Baillie Gifford American recovered after mid-September drop

What is clear is that there are different forces at play. Politically, there is no impetus to bring in a further financial stimulus package until the election is completed. Donald Trump will not introduce further measures until he is certain of his re-election, while Joe Biden will not extend a vastly popular measure among US voters, which was introduced by Donald Trump so close to the election. The issue of the actual running of the election and how it could play out, along with its ramifications, could be the subject of several other articles but suffice to say the markets can expect further inertia until January 2021 at the very least.

From an economic point of view, there is also the question about the capacity for further growth. Baillie Gifford American was one of the big winners following the recovery after lockdown. The fund held a position in Zoom, which saw a huge spike in users in April, May, June and beyond and subsequently saw its share price rise. But with talk of a second wave and the potential for ‘Zoom fatigue’, it is highly unlikely that tech stocks will be able to replicate the initial growth they saw earlier in the year. Where, for instance, will Zoom find a further 400 million global users?

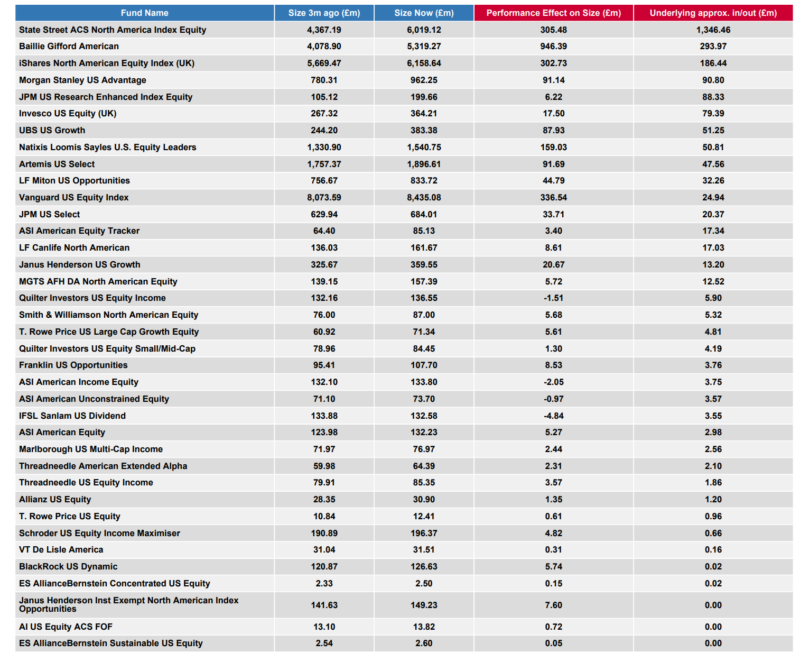

Looking ahead to 2021, we can be fairly confident that whoever is elected president, there will be further stimulus packages made available. The American economy, despite seeing huge job losses and a fall in productivity, has more than likely not even begun to see the full extent of the recession that most likely lies ahead. So with a further stimulus package on the cards, we can expect to see greater inflows into assets and funds. There will likely be a lot more money floating around the economy, but with consumers reluctant to spend, it seems fair to assume that many will turn to savings or investment. We are already seeing the start of this trend as the table below shows, where several renowned US funds have seen large inflows of assets over the past three months:

Funds attracting the most money in the North America sector over the last three months

Source: FE Fundinfo (to the end of September)

Whatever happens on 3 November, this election promises to be like no other, taking place in an economic environment like no other. US funds have promised a rare beacon of stability in volatile markets, but for how long they can continue, is unclear. Like 2020 as a whole, it all remains too uncertain.

Charles Younes is a research manager at FE Investments