Advisers look set to become the most expensive part of client’s total cost as they pester fund groups and platform providers to cut costs but remain stubborn on their own.

Though 90% of the 404 advice firms that took part in Lang Cat’s State of the Adviser Nation report say they have brought down the total cost of ownership (TCO) for clients, most have achieved this by putting pressure on investment firms to lower their fees.

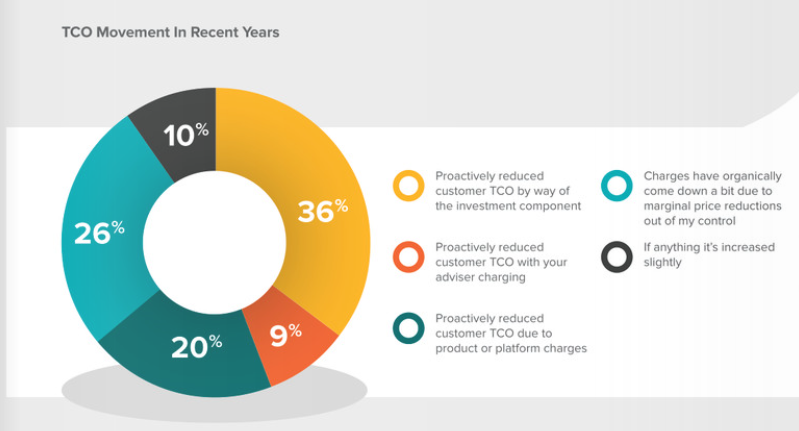

Only 9% of advisers have cut their own costs in recent years compared with 36% of respondents who have reduced costs by way of the investment component.

IFAs were also more likely to badger platform providers to trim their fees with 20% saying they achieved a lower TCO this way.

“While platform costs are falling, it is clear that most firms believe investment management should take the hit, with more fat to go after,” said Lang Cat founder and co-author of the report Mark Polson.

“While no one expects advisers to cut their own throats, it will soon be the case that advice is commonly the single most expensive element of TCO, and with new disclosures and disruptors in the market we think that price pressure will inevitably read across.”

Virtually no competition between advisers

Ten percent of advisers told the Lang Cat they had actually raised their fees in recent years.

“It’s a brave adviser that raises their costs in the current market environment, particularly as investment and platform charges fall,” Polson said.

But CWC Research managing director Clive Waller says IFA firms can do as they please because there is “virtually no competition between advisers”. “Like most pricing, you’ll take as much margin as you can, and advisers are no different to the rest of us.”

Boring Money founder and CEO Holly Mackay agrees “advice is not a competitive market today”.

“Costs are opaque, so comparison is nigh impossible; supply of advice is finite; and many advice firms report having enough clients so the external pressures on pricing are relatively muted.”

Hard to see how advisers could avoid raising fees

Investment providers have much larger margins than advisers meaning there is greater scope for them to cut fees, notes Martin Bamford, director of client education at Informed Choice.

Advisers meanwhile “face relentless cost pressure, including outrageous FSCS levies and professional indemnity insurance premiums”.

“With a high and rising cost burden, it’s hard to see how advisers could avoid raising their fees, let alone consider a fee cut,” he says.

It’s difficult to know how a bigger regulatory burden has translated into costs for advisers, says Waller, though he reckons the average adviser will spend between 6 to 7% on PI and other regulation costs.

What matters is ‘the whole bloody cost’

“People value people,” says Mackay, “so it will always be true that they will place a higher value on the person they talk to than the asset manager with a corporate brand at the end of the food chain.”

But she thinks advisers will eventually feel the squeeze as the evolution of the digital advice market ramps up and the regulator scrutinises opaque charging practices.

Waller thinks its nonsensical that the FCA demands transparency from asset managers when it comes to disclosing the total costs of their funds but doesn’t insist on this across the piece.

“The only thing that matters – it’s not the asset management costs; it’s not the IFA cost; it’s the whole bloody cost. Until the regulator gets that we’re not going to get very far.”

Waller says eventually the “sleepy” Financial Conduct Authority will have to get involved eventually as “the cost of decumulation is far too high”.

The typical adviser fee is “at the thick end” of 1%, while portfolio managers charge between 1% and 1.5%, meaning clients are paying between 2% and 2.5% in fees on average. “If you’re withdrawing at a rate of 4% that means half of your income or more is going in fees.”