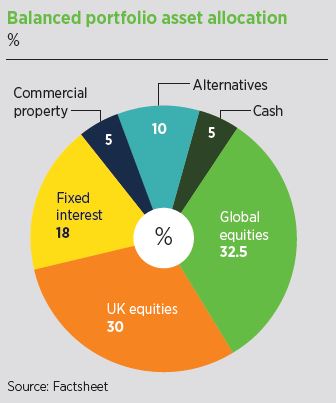

Allocation to UK equities has suffered in the Brewin Dolphin model portfolios of late in favour of the US, Europe and Asia, even though the domestic economy has started to show faint signs of a recovery.

In June, domestic retail sales jumped above pre-Covid levels and the Purchasing Managers Index (PMI) hit its highest level since the Brexit referendum, although Brewin Dolphin remains unconvinced.

The wealth manager’s latest asset allocation update notes retail sales account for only about one third of household spending, while the PMI surge is indicative of the fact the UK eased lockdown restrictions more recently than some.

There are other reasons the team is not favouring the UK. One is the make-up of the stock market, which Brewin Dolphin senior investment manager John Moore (pictured) says is largely services-based and heavily weighted to oil, mining and banking stocks.

“These are industries that have significant internal challenges, so the influence of such stocks at the top end of the market makes for a not necessarily immediately appealing market composition,” he says.

Sterling has rallied lately but the team believes that, because of Brexit, the currency is likely to be on the back foot over the longer term. And if there is a hard Brexit, it is likely to hit returns.

The team’s view on domestic equities is also recognition of the fact that sentiment is poor and valuations, accordingly, are not particularly demanding.

“We’re not throwing the baby out with the bath water but it just feels instinctively like there are better opportunities elsewhere, viewing things over 12, 18, 24 months,” says Moore.

The ‘wind is at your back’ in US equities

By contrast, despite a weaker dollar, the Brewin team thinks the US equity market has performed well on the back of continued strong performance from growth stocks, particularly healthcare and technology, bar the recent blip in the latter, which make up about 40% of the market.

“The wind is at your back as a result of that,” says Moore. He accepts there has been a degree of volatility in earnings for some American companies, but he sees more earnings growth opportunities coming from the US than elsewhere.

One big change with regard to the US recently has been a weakening of the dollar, and the team has discussed in-depth whether or not the currency has peaked.

“I suspect part of that is due to events of the past five months or so,” he says. “My guess is it over-earned in terms of how it performed because it is the reserve currency. In a crisis you go to the biggest pool of money, and therefore the dollar was probably a beneficiary of that in March, April and May.

“So there’s a gentle reversal of some of that activity. I suspect that will be a point of debate but I’m not visualising us becoming negative on the US.”

Moore predicts speculation over the dollar will heat up between now and the US presidential election on 3 November before settling down. The big question is whether the economy is strong enough to take Trump to a second term.

“The opinion polls would say that’s not likely and I think that’s the reading I see,” says Moore. “My view is that it will be a bit closer than everybody observes today.”

But the team is not making any specific moves ahead of the election. “There are times you can wade in and participate and other times you may just want to take a step back and observe.”

Not going against the earnings momentum

In the MPS, the team has Baillie Gifford American and JP Morgan US Equity Income, effectively proxies for growth and value, respectively, and it has spent a fair amount of time considering the right balance between the two. The portfolios also have exposure to Vanguard and Fidelity passive products.

“However compelling value has been on one side of the table it hasn’t been a helpful observation necessarily,” says Moore. “The problem for lower valuation stocks is that they need to demonstrate the ability to recover and improve earnings.

“Higher valuation stocks have the earnings momentum, so there’s less of an incentive for people to walk away.

“If you’re a big bull of the economic recovery, you can be more disposed to those value stocks and perhaps some of that sits elsewhere in the US, or elsewhere in the world, for example emerging markets. We don’t want to lean against the way the market is at present, against that momentum in earnings.”

Manufacturing bias makes Europe attractive

The team recently moved overweight Europe, which it funded by taking cash and going underweight UK.

Europe is attractive to Brewin because of the market’s blend of manufacturing and services, unlike the UK. This manufacturing bias means Europe stands to gain from a recovery by China, wider Asia and other areas that are further along the path to normality, argues Moore.

Eurozone exports to China as a share of GDP are much higher than for the US, the team notes.

Brewin’s latest asset allocation update points to the risk of an increase of Covid-19 cases, particularly in Spain. But Moore doubts this will mark a serious downturn, adding not all the steps being taking by authorities, for example more testing at airports, will slow growth.

He points to a long-term allocation to Threadneedle European Select, which has “served us well through different scenarios”.

Asia buoyed by rising wealth and tech innovation

When it comes to Asia, Moore accepts it hasn’t been firing on all cylinders during the past few years, but is attractive for its rising wealth and consumption, as well as its increasing innovation in technology.

“You can see what’s happened in China recently where it feels like there’s been a lot of innovation,” he says. “I’ve got three girls and TikTok just completely takes over their world.”

The region is also more advanced along the Covid timeline, he says. “They were early in and are earlier out, so, again, there is this natural ability to participate in some of that recovery and the growth.”

China/US relations remain a risk to the region but “we expect this is a wall of worry that Asia ex Japan equities will be able to climb”, says the firm’s asset allocation note.

The portfolios hold a basket of funds dedicated to the region, including Stewart Investors Asia Pacific Leaders, Hermes Asia ex Japan and Invesco Asia. It also holds the Fidelity Index Pacific ex Japan fund.

Keeping in credit

Moore says with bonds it is tricky to see where returns come from, especially when government debt yields have dropped to all-time lows and failed to rise on the back of stronger economic data.

That said, portfolios do have exposure to sovereign bonds due to their liquidity profile and because in times of volatility they are less sensitive to economic movements.

But the team has upped credit exposure. “It’s easier for us to be in line with credit because that is consistent with our overweight in equities generally,” says Moore.

Credit appeals because the team believes there are robust companies that can participate in the economic recovery. It also offers a pick-up in yield, which, again, is less the case with government bonds.

Moore believes active management is essential to this asset class as there is a high degree of inefficiency in corporate bonds. Within the MI Select funds, the team uses Pimco for UK credit and Robeco for global exposure.

Zero property exposure may have been better in hindsight

The team is also underweight property, at 2.5% versus the benchmark’s 5%, although Moore admits that in hindsight zero exposure may have been better.

“We recognise there are some diversification benefits to property and the approach we’ve got has been typically Reit and overseas based, so it doesn’t plug itself into the UK high street and can have exposure to assets like data centres.”

Moore names Schroder Global Cities as one of the ways the team is exposed to the asset class.